6 Ways Nonprofit Retirement Plans Are Changing Mar 27, 2024Some provisions of 2022’s SECURE Act 2.0 (a follow-up to the SECURE Act of 2019)... read more

Consider an IRA if You’re Married and Not Earning Compensation Jun 26, 2023When one spouse in a married couple is not earning compensation, the couple may not be... read more

Retirement Plan Early Withdrawals – What to Know Feb 1, 2023Most retirement plan distributions are subject to income tax and may be subject to an... read more

SECURE 2.0 – Here’s What You Need to Know Jan 9, 2023A new law was recently signed that will help Americans save more for retirement,... read more

A Solo 401(k) Plan for the Self-Employed Aug 25, 2022Do you own a successful small business with no employees and want to set up a retirement... read more

Your Retirement Plan, Third-Party Providers and You Sep 7, 2021Jen: This is the PKF Texas - Entrepreneur’s Playbook®, I'm... read more

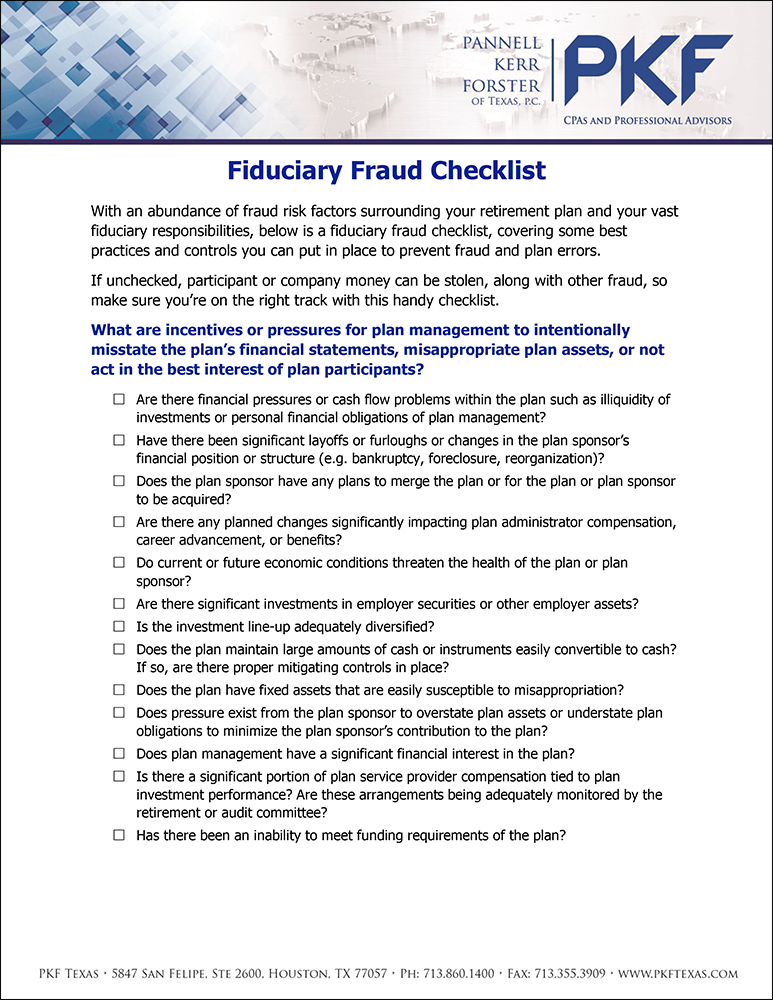

Download Now: Fiduciary Fraud Checklist Jan 26, 2021Several of our clients have inquired about a fraud checklist they can use for their... read more

How to Keep Retirement Plan Fees in Check Dec 8, 2020There has been a trend of increased litigation over the reasonableness of retirement... read more

What is a Coronavirus-related Distribution? Jun 23, 2020As you may have heard, the Coronavirus Aid, Relief and Economic Security (CARES) Act... read more

How CARES Act Changes Retirement Plan and Charitable Contribution Rules Apr 8, 2020As we all try to keep ourselves, our loved ones and our communities safe from the... read more