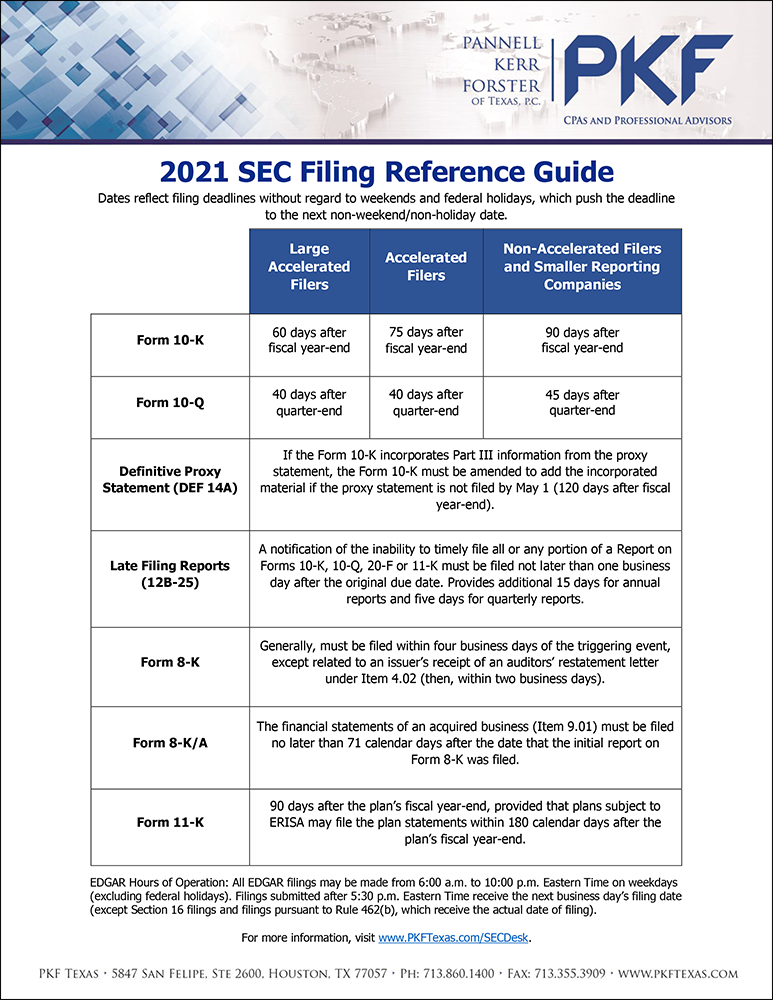

The 2021 SEC Filing Reference Guide is Available! Jan 18, 2021We have updated our website's SEC Desk with the 2021 SEC Filing Reference Guide, which... read more

Recap: Accounting and SEC Reporting Update Zoom Webinar Dec 11, 2020Deemed as a riveting presentation from a CFO and SEC registrant attendee, PKF Texas... read more

EDGAR System Upgrade No Longer Supports 2018 GAAP Taxonomy Jul 2, 2020The Securities and Exchange Commission (SEC) announced on June 29, 2020 that the EDGAR... read more

SEC Disclosure Effectiveness Initiative and What it Means for Public Companies Apr 6, 2020Jen: This is the PKF Texas Entrepreneur’s Playbook, I'm Jen... read more

Monitoring the FCPA: Is Your Public Company in Compliance? Mar 30, 2020Jen: This is the PKF Texas Entrepreneurs Playbook. I'm Jen... read more

PCAOB and SEC: Possible Merger by 2022? Mar 24, 2020Jen: This is the PKF Texas Entrepreneur’s Playbook. I’m Jen... read more

How Critical Audit Matters (CAMs) Affect SEC Companies Mar 9, 2020Jen: This is the PKF Texas Entrepreneur's Playbook, I'm Jen... read more

How Comment Letter Trends from the SEC Impact Public Companies Mar 2, 2020Jen: This is the PKF Texas Entrepreneur's Playbook. I'm Jen... read more

SEC Proposes Disclosure Changes to Regulation S-K Feb 19, 2020As part of their Disclosure Effectiveness Initiative, the Securities and Exchange... read more

Public Statement from SEC Chairman: Amendments, Initiatives, more Feb 5, 2020On January 30, 2020, Chairman of the Securities and Exchange Commission (SEC), Jay... read more