Protect Your Nonprofit from Holiday Season Fraud Nov 19, 2024Key Points Prevent cash theft at events with supervised management and credit card... read more

Preventing Fraud in Your Youth Sports League Jun 5, 2023A few years ago, the popular and well-compensated executive director of a west coast... read more

4 Best Practices for Your Fraud Recovery Plan Mar 24, 2023According to the Association of Certified Fraud Examiners (ACFE), not-for-profit... read more

Beware Disaster Fraud for Your Not-for-Profit Oct 6, 2022It’s been a busy year for natural disasters, with Hurricane Ian only the latest calamity... read more

Sharing Your NFP’s Values and Limit Fraud Losses Aug 26, 2022Every two years, the Association of Certified Fraud Examiners releases its Report to the... read more

4 Key Tips in Limiting Fraud in Not-for-Profits Jun 20, 2022Recently, the Association of Certified Fraud Examiners (ACFE) published its biannual... read more

Mitigating the Risk of Commission Fraud Jan 3, 2022Many employees — from retail workers to sales staffers involved in complex... read more

Does Your Not-for-Profit Have an Internal Controls Gap? Sep 1, 2021The typical defrauded not-for-profit loses $75,000 per fraud incident, according to the... read more

How Your Not-for-Profit Can Recover from Fraud Feb 25, 2021Thousands of not-for-profit organizations fall victim to embezzlement schemes every year... read more

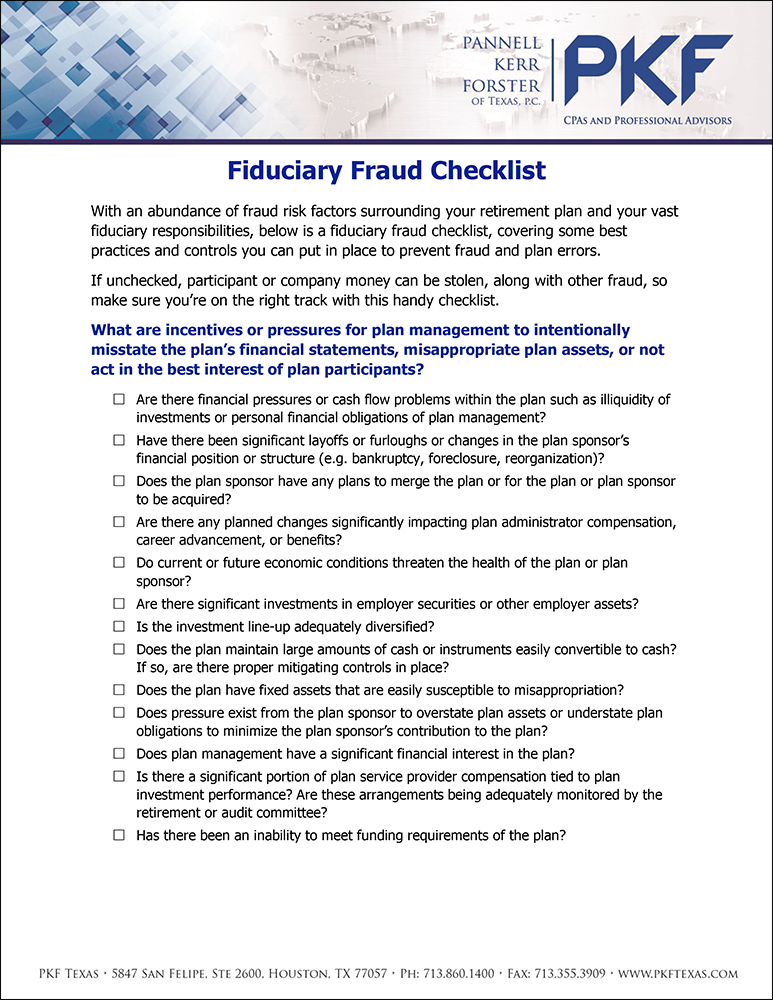

Download Now: Fiduciary Fraud Checklist Jan 26, 2021Several of our clients have inquired about a fraud checklist they can use for their... read more