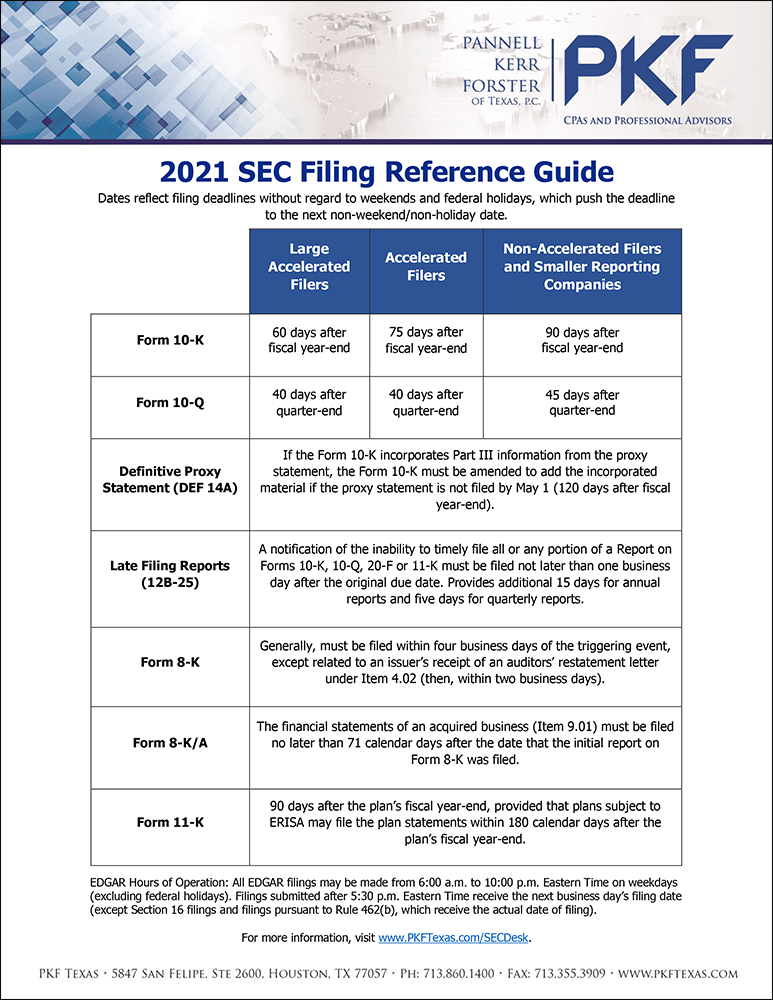

The 2021 SEC Filing Reference Guide is Available! Jan 18, 2021We have updated our website's SEC Desk with the 2021 SEC Filing Reference Guide, which... read more

Amendments to Regulation S-K Help Simplify Disclosure Compliance Nov 5, 2020The Securities and Exchange Commission (“SEC”) recently issued Final Rulemaking Release... read more

EDGAR System Upgrade No Longer Supports 2018 GAAP Taxonomy Jul 2, 2020The Securities and Exchange Commission (SEC) announced on June 29, 2020 that the EDGAR... read more

Maintaining Independence: Navigating SEC and PCAOB Guidance Mar 16, 2020Jen: This is the PKF Texas Entrepreneur’s Playbook. I’m Jen... read more

How Critical Audit Matters (CAMs) Affect SEC Companies Mar 9, 2020Jen: This is the PKF Texas Entrepreneur's Playbook, I'm Jen... read more

How Comment Letter Trends from the SEC Impact Public Companies Mar 2, 2020Jen: This is the PKF Texas Entrepreneur's Playbook. I'm Jen... read more

SEC Proposes Disclosure Changes to Regulation S-K Feb 19, 2020As part of their Disclosure Effectiveness Initiative, the Securities and Exchange... read more

Proposed Rules from SEC Impact Proxy Advisory Firms and Shareholder Voting Dec 4, 2019In response to the transparency issues around proxy advisory firms, the Securities and... read more

Trends Emerging from the PCAOB Annual Inspection Report Nov 18, 2019Jen: This is the PKF Texas Entrepreneur's Playbook. I'm Jen... read more

What FINRA Finds in Your Expense Sharing Agreements Nov 11, 2019Jen: This is the PKF Texas Entrepreneur's Playbook. I'm Jen... read more